.jpg)

Your Guide to the Centrelink Home Equity Access Scheme

The great Australian dream has always been to own your own home outright without the encumbrance of a loan and mortgage repayments. A home provides many things like a roof over your head, security and a place to raise a family. For the majority of Australians in their senior years it is also their largest asset, which often can mean they are asset rich and cashflow poor. Australian residential property has grown an astonishing 382% over the past 30 years (Core Logic, 2022), which results in large amounts of untapped equity.

How can you unlock cashflow from your home?

There are a number of ways that retirees can take advantage of this untapped equity and turn their largest asset into an income stream, mainly;

Downsizing

The most obvious option for retirees wanting to free-up cashflow in their home is to sell their current property and purchase something of lesser value. The difference in price is cash they could invest to earn an income or make use of the downsizer contribution to Super, and start/add to an account-based pension.

This option can make sense if you are wanting to downsize from a larger property into something smaller that requires less ongoing maintenance.

This is not always a favoured option if you are wanting to stay in your current home. There are also costs for stamp duty, agent fees and moving will be incurred.

Reverse Mortgage

A reverse mortgage can be an option for those wanting to use equity in their homes to start a regular income stream, take a lump sum or a combination of the two. A reverse mortgage allows you to borrow money using

the equity in your home as security. The Lender will allow you to borrow in between 15%-25% of the value of your home, depending on your age (60+). A reverse mortgage allows for greater flexibility in how much equity you can use as an income stream or lump sum, but usually attracts a higher interest rate on the loan.

Home Equity Access Scheme (HEAS)

Home Equity access scheme (HEAS) is essentially a reverse mortgage administered by Services Australia. Australian’s who are aged pension age (67+) can offer their Australian property as security to access a loan from the government to supplement their cashflow needs. The loan takes the form of a series of fortnight payments and/or advance lump sums. The benefit of HEAS through the government is the interest rate of 3.95% compounded fortnightly, which is much lower than other commercial reverse mortgages.

Who can get it?

You must meet certain eligibility requirements to access the HEAS. You must meet all of the following;

- you or your partner are Age Pension age or older

- you get or are eligible to get a qualifying pension

- you or your partner own real estate in Australia you can use as security for the loan

- you or your partner, or any co-owner of the property, aren’t bankrupt or subject to a personal insolvency agreement

- you have adequate and appropriate insurance that covers the real estate offered as security.

Can you get Home Equity Access Scheme loan payments if you don't get Age Pension payments?

Services Australia will consider you eligible if you meet the qualifying rules for a one of the qualifying pensions (age Pension, Carer Payment or Disability Support Pension) but you don’t get a payment because your rate is zero – for example if your income or assets is over the threshold. Essentially meaning that you can apply for the HEAS even if you don’t receive the Age pension due to your income and/or assets being too high.

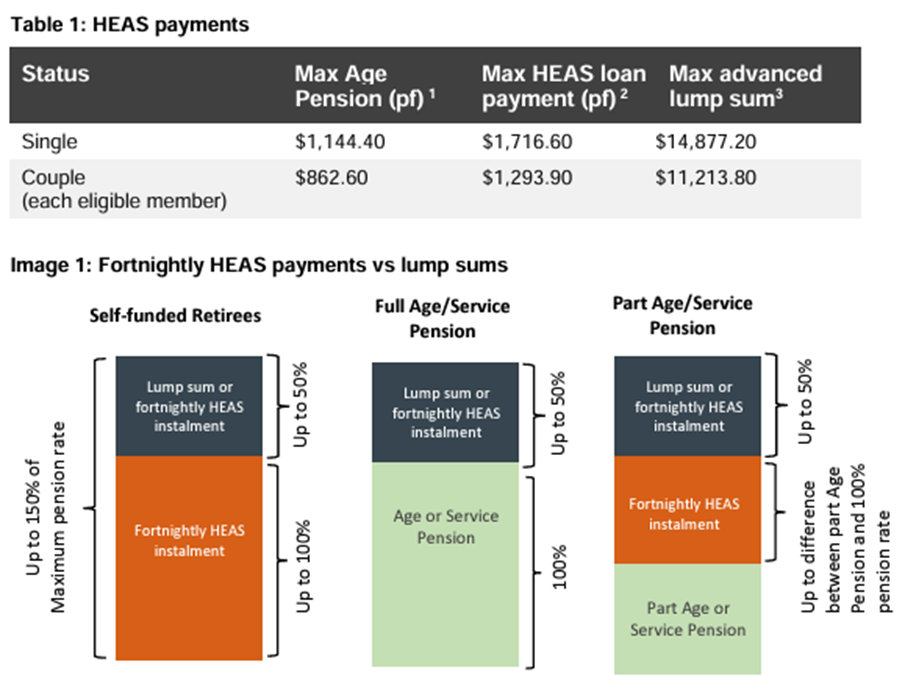

How much can you get?

How much you can get from the HEAS will depend on whether you receive the Age Pension on not. It will also depend on how you choose to get your loan from these options;

- a fortnightly amount

- an advanced payment of the loan as a lump sum

- a combination of both

Services Australian will pay your loan payment until you reach the maximum loan amount (MLA).If you choose to take an advanced payment, this may reduce the fortnightly loan amount you can get for 26 fortnights.

Source – MLCTechnical

- Rates current 20 September 2024. Includes Basic rate + maximum Pension Supplement + Energy Supplement. This amount may vary if the client is also eligible for rent assistance.

- 150% of the fortnightly maximum pension rate (MPR).

- 50% of the maximum annual age pension rate.

If you get a pension

Your combined loan and pension payment each fortnight can’t be more than 150% (1.5 times) of your maximum pension rate (MPR).

Example 1 – Full Age Pension

Bill and Melinda receive the Full age pension and have a Maximum Pension rate (MPR) of $862.60 each per fortnight including Pension and Energy supplements. Bill and Melinda can only receive a total of 150% of the MPR.

$862.60 x 150% = $1,293.90

This means that their maximum total payments including Age pension will be $1,293.90 each per fortnight. Therefore their HEAS payments will be;

$1,293.90 – $862.60 = $431.30 each per fortnight

Example 2 – Part Age Pension

Tom and Rita receive a part-age pension of $593.63 per fortnight each. Their maximum pension rate is $862.60 p/ft each.

Tom and Rita can only only receive a total of 150% of the MPR.

$862.60 x 150% = $1,293.90

This means that their maximum total payments including Age pension will be $1,293.90 each per fortnight. Therefore their HEAS payments will be;

$1,293.90 – $593.63 = $700.27 each per fortnight

If you don't get a pension

If you don’t get a pension you can still get a loan under the HEAS. You can get a fortnightly loan payment up to the full 150% of the maximum rate of your qualifying pension. If you are Age Pension age or older, your qualifying pension will be the Age Pension.

Example – Self-Funded Retiree

Elon is a self-funded retiree who meets the qualifying rules for the Age Pension, however his financial assets exceed the asset test for a single homeowner and hence his payment rate is zero.

Elon can receive HEAS payments equivalent to 150% of the MPR.

$862.60 x 150% = $1,293.90

This means that his maximum total payment will be $1,293.90 each per fortnight.

$1,293.90 – $0 = $1,293.90 each per fortnight

What is the interest rate for Home Equity Access Scheme?

The current annual interest rate that is charged by Services Australia is 3.95% that compounds fortnightly on the HEAS loan Balance.

The interest rate is set by the minister of Social Services. Services Australia will tell you if it is going to change.

Example – Loan balance calculation

Jeff gets his first fortnightly loan payment of $750 from HEAS. Interest on this amount will accrue straight away. At the end of the first fortnight, Jeff’s loan balance is $751.14. George then gets another $750 loan payment. We charge interest on the total loan balance, including interest charged on previous loan payments.

At the end of the second fortnight, George’s outstanding loan balance is a total of all of these. His:

- first loan payment plus interest, which totals $751.14

- second loan payment, which is $750

- interest on the balance of $1,501.14, which is $2.28.

That makes his new outstanding loan balance $1,503.42.

Compounding interest and home growth

The compounding interest on the HEAS is usually an area of concern for most that we have helped access the scheme. What needs to be kept in mind is that while the interest is being compounded at 3.95% and the loan balance grows over time, the home value should grow over time as well. Historically, Australian home prices have grown in compounding terms 5.4% on average since July 1992 (Core Logic, 2022)

How can I see how much I can borrow?

To see how much you can borrow, you can use the HEAS calculator on the Centrelink website or contact one of our knowledgeable advisers at P3FP to run a calculation and talk you through options.

Final Thoughts

The Home Equity Access Scheme through Services Australia can be an excellent solution for seniors looking for additional income, by converting home equity into a stable income stream. The HEAS loan can be used for lump sum needs like renovations or can be taken as a fortnightly sum which may alleviate some pressure on withdrawals from Superannuation pensions or just add to your Age Pension income.

While it is less flexible that a commercial reverse mortgage, the favourable interest rate makes this option very appealing.

The information in this communication is factual in nature. It reflects our understanding of existing legislation, proposed legislation, rulings etc as at the date of issue, and may be subject to change. While it is believed the information is accurate and reliable, this is not guaranteed in any way. Examples are illustrative only and are subject to the assumptions and qualifications disclosed. Whilst care has been taken in preparing the content, no liability is accepted for any errors or omissions in this communication, and/or losses or liabilities arising from any reliance on this communication.