The Great Debate: Shares vs Property

Shares vs Property – the great debate that has often left investors divided. Both investment options have their pros and cons, making it difficult for investors to decide which is better for them.

When it comes to shares, the potential for high returns is often touted. The stock market is known for its ability to generate significant wealth, particularly when investing in thriving companies. However, it also carries a level of volatility that can leave investors on edge.

On the other hand, property investment offers stability and tangible assets. Real estate is often seen as a safe bet, providing a steady income stream and potential long-term growth. However, it requires significant upfront capital, and there are associated costs and risks involved.

So, which investment wins in this great debate? The answer ultimately depends on an individual’s financial goals, risk appetite, and investment timeframe. The advisers at P3FP firmly believe that both investments play significant roles in wealth building. In this article I aim to provide an unbiased assessment of the pros and cons of shares and property, allowing you to make a more informed decision based on your unique circumstances.

Overview of shares as an investment

Investing in shares, also known as stocks or equities, involves purchasing a portion of a publicly traded company. When you own shares, you become a shareholder, and you have a claim on the company’s assets and earnings. The stock market, where shares are bought and sold, offers investors the opportunity to participate in the growth and success of various businesses.

The stock market is a dynamic and complex ecosystem, with share prices constantly fluctuating based on a variety of factors, including the company’s financial performance, market trends, and investor sentiment. Investors can buy and sell shares through stockbrokers or online trading platforms, and they can choose from a wide range of investment strategies, such as long-term buy-and-hold, short-term trading, or diversified portfolio management.

Shares can provide investors with the potential for capital appreciation, as the value of the shares may increase over time, and they can also generate income through dividend payments. Dividends are a portion of a company’s profits that are distributed to shareholders, and they can provide a steady stream of income for investors.

Advantages of investing in shares

Would you like to be an owner of a massive business like Apple or Microsoft? The share market gives the public the ability to purchase equity in listed companies, allowing investors to participate in the hard work of these businesses, while you sit at home. Owning shares in a company allows you to passively participate in a company’s success, the growth in their share price and the distributions of the profit in the form of dividends.

In Australia, we also get the benefits of Franking Credits, which offsets the effects of double taxation on company earnings. Franking credits can help to reduce the tax liability on dividends if your personal tax rate is below the 30% company tax rate. This is important for your Superannuation fund with a headline tax rate of 15% and for retirees who have a tax rate of 0%. In the scenario where your personal tax rate is 0%, you would actually receive these franking credits as a refund. Many retirees depend on these franking credit refunds as a booster for their income each year.

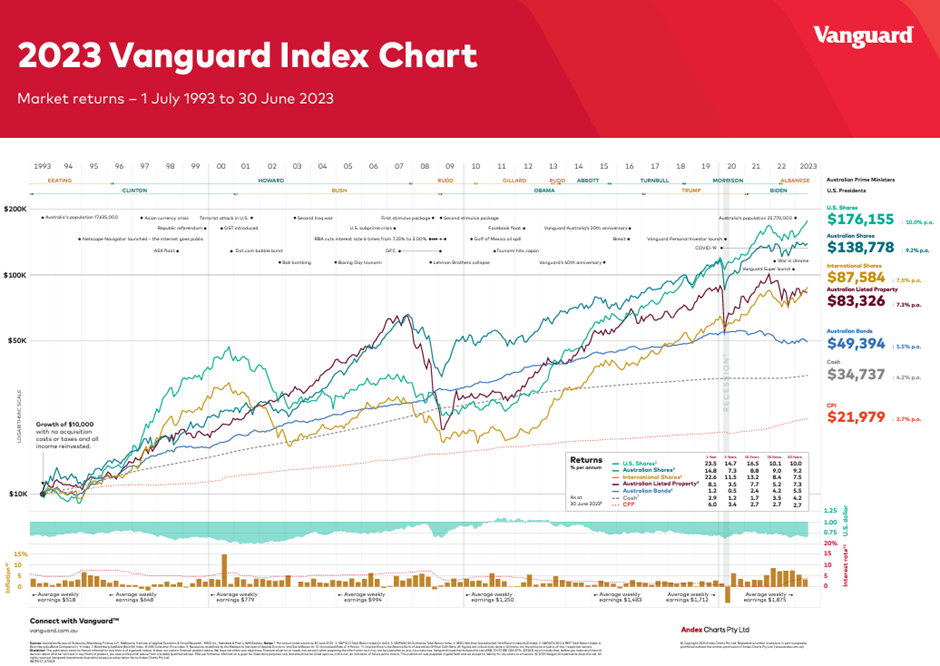

The stock market has historically delivered impressive long-term returns, with the average annual return of the S&P 500 index, a widely followed benchmark for the US stock market, being 10% over a 30-year period (1993-2023). The local market in Australia while returning slightly less than the US market, the ASX All Ordinaries (total return index) still provided similarly impressive results for investors with an average annual return of 9.2%. It should be noted that the figures stated and represented in the chart below from Vanguard, are total return figures inclusive of dividends.

Figure 1: 2023 Vanguard Index chart (Source: Vanguard)

Another advantage of investing in shares is the ability to diversify your portfolio. By investing in a variety of companies across different sectors, investors can reduce their overall risk exposure and potentially mitigate the impact of any single investment performing poorly. Diversification is a key principle in portfolio management, as it helps to spread out the risk and potentially enhance the overall returns.

You can also easily add to your investments, purchasing new shares or using a dollar cost average strategy to build you portfolio. This is an advantage over property where a large investment is required to purchase a new property.

Investing in shares also offers investors a high degree of liquidity. Unlike other asset classes, such as real estate, shares can be bought and sold relatively quickly and easily, allowing investors to access their funds when needed. This flexibility can be particularly beneficial for investors who may need to access their capital in the short-term or who want to rebalance their portfolio as market conditions change.

Risks associated with investing in shares

While investing in shares can offer the potential for high returns, it also carries a significant level of risk. One of the primary risks associated with shares is market volatility. The share market can be highly volatile, with share prices fluctuating rapidly in response to a variety of economic, political, and company-specific factors. This volatility can lead to short-term losses, and it can be particularly challenging for investors who are not comfortable with the level of risk involved.

Another risk associated with investing in shares is the risk of individual company failure. Not all companies are successful, and some may even go bankrupt, resulting in a complete loss of the investor’s capital. This risk is particularly relevant for investors who are not diversified and who have a concentrated portfolio in a small number of companies.

Overview of property as an investment

Investing in property, or real estate, involves the purchase of land, buildings, or other types of real estate with the intention of generating income or capital appreciation. Property investment can take many forms, including residential properties, commercial or industrial properties.

The property market is often seen as a more stable and predictable investment option compared to the stock market, as real estate is a tangible asset that can provide a steady stream of rental income and the potential for long-term capital growth. Property investors can generate income through renting out their properties, and they can also benefit from the appreciation in the value of their properties over time.

Investing in property requires a significant upfront capital investment, as well as ongoing costs such as maintenance, taxes, and insurance. However, many investors view property as a more secure investment option, as it provides a physical asset that can be leveraged or used as collateral for loans.

Advantages of investing in property

One of the primary advantages of investing in property is the potential for stable and consistent income. When a property is rented out, the investor can receive a regular stream of rental payments, which can provide a reliable source of passive income. This can be particularly attractive for investors who are looking for a steady and predictable return on their investment. These rental payments can be inflation protected if set up correctly in lease agreements, where owners can index rents to CPI each year to ensure that the rental income isn’t devalued by inflation over the term of the lease agreement.

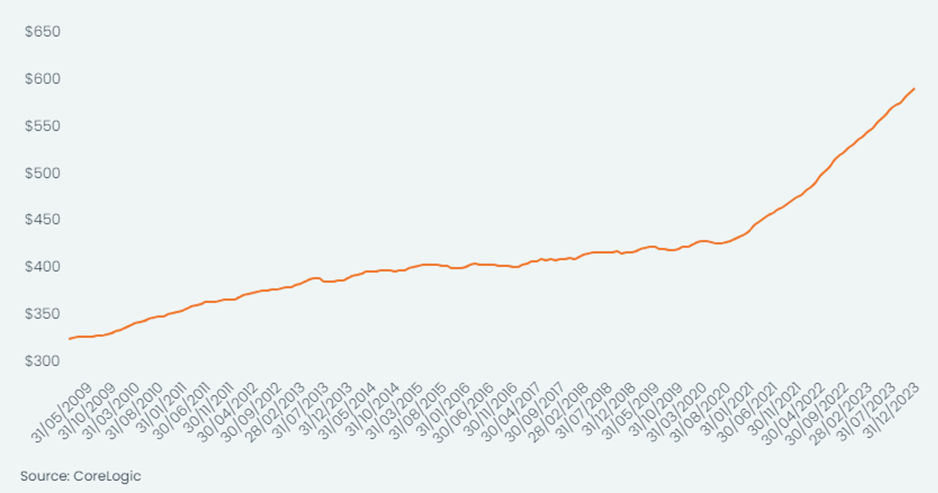

The graph from CoreLogic presented below in figure 2 below, shows the increase in average weekly rents for national dwellings.

Figure 2: Median weekly rent value (reported monthly, national dwellings)

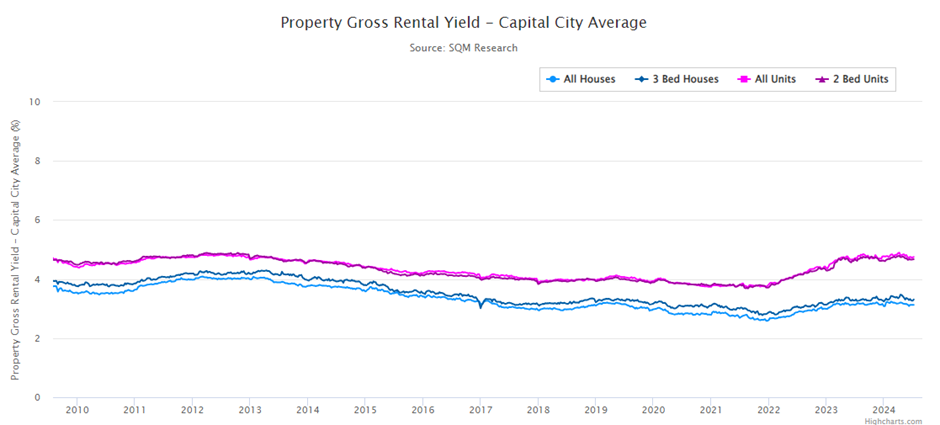

Rental yields have been steady over the years, although declining to date. This is illustrated in Figure 3 below from SQM Research. Declining yields over the years is understandable, as yield is simply a function of rent and increasing house prices (Yield = Rent / Property Price).

Figure 3: Property Gross Rental Yield – Capital City Average

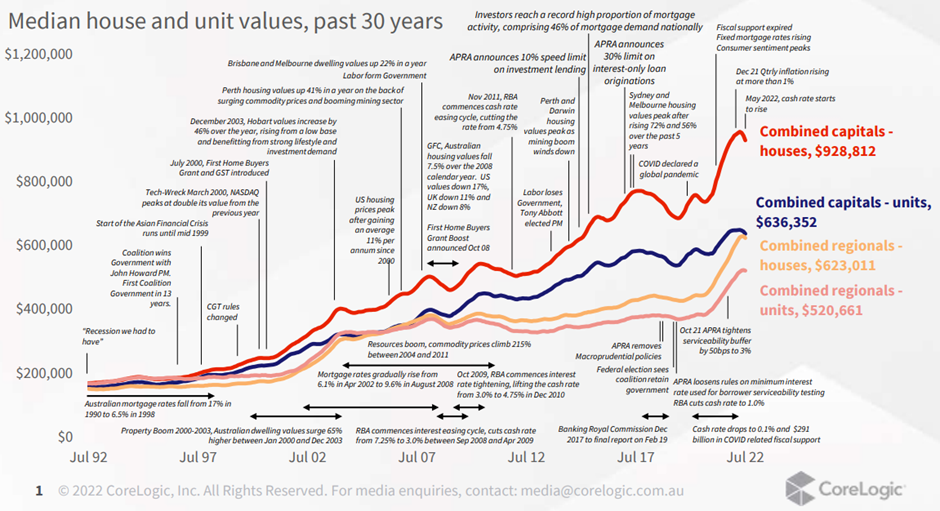

Another advantage of investing in property is the potential for long-term capital appreciation. Over time, the value of a property can increase, providing the investor with a significant return on their initial investment. This can be particularly beneficial for investors who are looking to build wealth over the long-term. See figure 3 below from CoreLogic, which illustrates the past 30 years of Median and house and unit values (1992-2022).

Figure 4: Median house and unit values, past 30 years (Source: Core Logic)

Investing in property also offers investors the ability to leverage their investment. By taking out a mortgage or other form of financing, investors can purchase a property with a relatively small down payment, and then use the rental income to cover the mortgage payments and other expenses. This can amplify the potential returns on the investment, but it also carries additional risks.

Further to this, investing in property provides the investor the ability to leverage the equity that has been built in the property over time. Banks are willing to lend additional money to property investors for further investments, as they can hold the property/ies as security while the loans are paid down. This can be a powerful wealth building strategy to leverage existing equity into buying further investment properties.

Risks associated with investing in property

One of the primary risks associated with investing in property is the illiquidity of the asset. Unlike shares, which can be bought and sold relatively quickly, property transactions can take a significant amount of time and can be subject to various legal and administrative processes. This can make it difficult for investors to access their capital when they need it, which can be a particular challenge in times of market volatility or personal financial emergencies.

Another risk associated with investing in property is the potential for unexpected expenses. Property ownership comes with a range of ongoing costs, including maintenance, repairs, taxes, and insurance. These costs can add up quickly and can eat into the investor’s returns, particularly if the property experiences unexpected issues or if the market conditions change.

Renting your property can bring with it additional risks. You could find yourself in a position where you are renting to a bad tenant, or find that for periods you might not be able to find a tenant to rent the property.

Investing in property also carries the risk of market fluctuations. The value of a property can be affected by a variety of factors, including local economic conditions, changes in interest rates, and changes in government policies and regulations. This can make it difficult for investors to predict the future value of their investment, and can lead to significant losses if the market conditions change in an unfavourable way. The advantage here is that property may have over shares is that daily property values are largely unseen, where share prices are updated daily. Hence there is less perceived volatility, but the market mechanisms of supply and demand work in a very similar way.

Comparing the returns of shares and property

When it comes to comparing the returns of shares and property, it’s important to consider a range of factors, including the investment timeframe, the level of risk involved, and the potential for capital appreciation and income generation.

In general, the Australian stock market and Australian property market have historically delivered fairly comparable returns. Over the long-term, the average annual return of the ASX All Ordinaries Total Return index is around 9.20%, and the US S&P 500 index 10% (Source: Vanguard), while the average annual return of the Australian housing market has been around 9.7% (Source: REIA). This suggests that investing in property or shares can yield similar outcomes.

Conclusion

In conclusion, the debate between investing in shares or property is a complex one, with bothinvestment options offering their own unique pros and cons. The table below summarises the pros and cons discussed in this artcle;

Table 1: Pros and Cons of Property and Shares

Ultimately, the decision of which investment to choose will depend on an individual’s financial goals, risk tolerance, and investment timeframe.

Investors who are comfortable with a higher level of risk with the benefit of greater flexibility may be more inclined to invest in shares, while investors who are seeking a reliable source of passive income and are willing to take on the additional costs and responsibilities of property ownership may prefer to invest in real estate.

Regardless of the investment choice, it’s important for investors to do their due diligence, research the market conditions, and seek professional advice to ensure that they are making informed and well-considered investment decisions. By carefully weighing the pros and cons of each investment option, investors can make a more informed decision and potentially achieve their financial goals.

My final thought is, sometimes it is not a decision to do one or the other. Often we say if you can, do both!

If you would like to discuss investing in shares, property or both, follow the link below to book a book a free consultation with one of our experienced advisers.

Disclaimer: The information in this article is general and does not consider your particular circumstances. We recommend specific tax or legal advice be sought before any action is taken and refer to the relevant Product Disclosure Statement before investing in any product. P3 Financial Planning Pty Ltd ABN 61 009 883 292 AFSL 464628