Retiring in a cost of living crisis? How to Navigate Record-High Costs with Confidence

Retirement is a milestone we all look forward to. It’s a time to swap the daily grind for travel, hobbies, and quality time with family. However, the latest data in a media release from the Association of Superannuation Funds of Australia (ASFA), has sent a clear signal to every Australian planning their future: the price of comfort has never been higher. For the first time in three years, the recommended superannuation lump sums have jumped significantly, with singles now needing $630,000 (up from $595,000) and couples requiring $730,000 (up from $690,000) for acomfortable lifestyle.

This isn't just a marginal increase, it’s a reflection of a perfect storm of economic pressures. While general inflation (CPI) sits at 3.8%, the costs of the specific goods and services retirees rely on most are climbing much faster. Electricity prices have surged by 21.5%, coffee and tea are up 15.3%, and even domestic travel has climbed by nearly 10%. Compounding this is the reality that the Age Pension hasn't kept pace with these essential costs, and with deeming rates set to rise in March 2026, many retirees may see their Centrelink support reduced just when they need it most. As these figures reach all-time highs, the message for pre-retirees is urgent: simply "having super" isn't enough anymore. You need a targeted strategy to manage your capital against these mounting pressures.

The New Retirement Reality

At our practice, we work closely with pre-retirees and retirees, particularly those navigating the complex intersection of private savings and Centrelink eligibility. We see first hand how market volatility and the cost-of-living squeeze can create anxiety for those living on a fixed nest egg.

The challenge isn't just the size of your capital; it's the liquidity and structure of that capital. Without a plan, you risk the "sequence of returns" trap, being forced to sell down your investments when the market is low just to pay your surging electricity bill.

The "Three Bucket" Strategy: Our Approach to Certainty

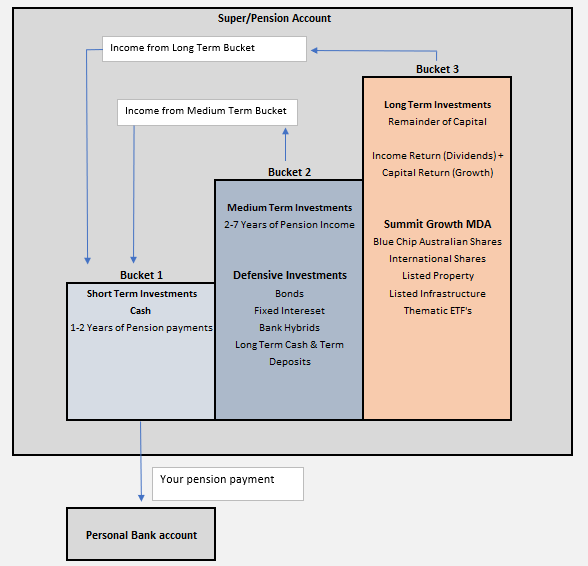

One of the most effective ways we help our clients manage rising costs while minimizing stress is through the “Three Bucket Strategy”. Instead of viewing your savings as one big, fluctuating pool, we segregate your assets into three distinct "buckets" based on your timeline for needing the cash.

Bucket 1: The Cash Reserve (Short-Term / 0–2 Years)

This bucket consists of liquid assets like cash and term deposits. It holds enough money to cover your living expenses for the next one to two years.

- The Benefit: Because this money isn't exposed to market fluctuations, you have total certainty of cash flow. Even if the share market drops tomorrow, your lifestyle remains unaffected because your next two years of income are already in the cash.

Bucket 2: The Defensive Growth (Medium-Term / 3–7Years)

This bucket holds more conservative investments, such as fixed interest, Term Deposits and Bonds.

- The Benefit: This bucket serves two purposes. The income derived from these investments are paid to cash, effectively topping up Bucket 1 (Short term). It also acts as a buffer. When Bucket 1 starts to run low, we can choose to refill it from Bucket 2. It offers higher returns than cash but with significantly less volatility than the pure share market, providing a bridge to your long-term wealth.

Bucket 3: The Growth Engine (Long-Term / 7+ Years)

This is where your long-term wealth sits, typically invested in Australian and international shares, property, and infrastructure.

- The Benefit: Growth assets are essential to combat inflation over a 20-30-year retirement. Because you have Buckets 1 and 2 to live off, you can afford to let Bucket 3 ride out market cycles without ever being a forced seller during a downturn. The income derived from the investments in Bucket 3 also pay to cash which tops up bucket 1 for your pension payments. Periods where growth returns are much higher than expected, this bucket can also be trimmed by taking profits to top up bucket 1.

This bucket strategy is a key differentiator to how money can be managed with an adviser vs how money is typically managed in an Industry super fund. In an Industry super fund, income is draw down directly from the pool of investments. This can cause “sequencing risk” where you may need to sell down assets to fund your income payments at the wrong time i.e. in a market correction. Over time this can have a large compounding impact on your retirement savings as that capital drawn does not have the opportunity to recover.

Maximizing Your Entitlements

For our clients with SMSFs and retail super funds, the Three Bucket strategy allows for incredible flexibility. You have the power to decide exactly which assets fund your buckets, allowing for sophisticated tax-effective income streams.

Furthermore, many retirees don’t realise that even with a healthy super balance, you may eventually become eligible for a part-Age Pension. Navigating the assets and income tests is becoming more complex, especially with the upcoming rise in deeming rates (to 1.25% and 3.25%). Our role is to ensure your capital is managed in a way that maximizes your eligibility for Centrelink, providing a vital, CPI-indexed safety net that helps offset the rising costs highlighted in the ASFA report.

Plan Ahead, Retire Happy

The ASFA Retirement Standard update is a wake-up call, but it’s not a cause for panic. It is a reminder that proactive planning is the difference between "just getting by" and a retirement of genuine comfort.

Whether you are five years away from finishing work or already enjoying yourretirement, now is the time to review your strategy. Are your assets structured to withstand 21% jumps in energy costs? Do you have a "cash bucket" to protect you from the next market dip?

Let’s secure your future together. If you’re looking for clarity on your Super strategy or want to see if you’re on track for a comfortable retirement in 2026 and beyond, we invite you to book a consultation with our team.

Disclaimer: This article contains general information only and does not take into account your personal objectives, financial situation, or needs. Before making any financial investment or planning decisions, you should give consideration to these matters and seek professional advice.