The Federal Government's major tax reform Bill covering the CGT discount, negative gearing, and several other measures from the 2026–27 Budget, has passed both Houses of Parliament on 25 June 2026 and now awaits Royal Assent. Once assented, these changes move from proposed to law. A separate trust tax measure and the definition of a "new build," are still being worked through.

Back in May we walked through the proposed Budget changes when they were just announcements. That's no longer the case for most of them. Below, we've updated our earlier summary so you know exactly what's now locked in, what's new since May, and what still deserves a wait and see.

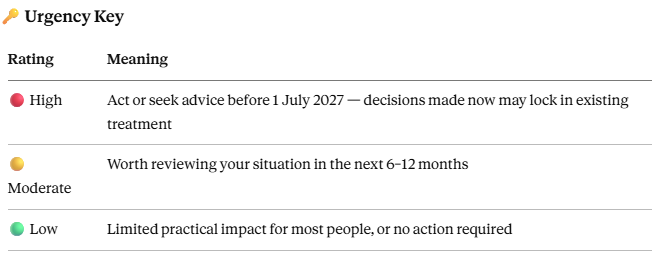

We've kept the same urgency system as our last article so you can scan for what actually needs a conversation with your adviser or accountant, versus what can wait.

Important: This is general information only and does not constitute financial advice. Please speak with your adviser or accountant before making any decisions based on this update.

Has the CGT discount actually changed? (CGT Discount Changes Explained)

Start date: 1 July 2027 - now law (pending assent) Urgency: 🔴 High

Yes, this is now legislated, not just proposed. From 1 July 2027 the 50% CGT discount is replaced by cost base indexation (adjusting your purchase price for inflation using CPI) plus a minimum 30% tax rate on the net capital gain calculated under that method.

What's confirmed:

- Assets you already own are split at 1 July 2027 via a deemed sale and reacquisition. The gain up to that date keeps the current 50% discount; the gain after that date is taxed under the new indexation method, subject to the 30% minimum.

- The 30% minimum only applies to the post-1 July 2027 portion of the gain not to the deferred, pre-2027 amount.

- You don't need a valuation done right now. You'll determine the 1 July 2027 value, either via a formal valuation or an ATO apportionment formula when you actually lodge the return for the year you sell.

- The 12-month holding rule looks through the deemed sale and reacquisition, so continuous ownership is what counts, not the post-2027 holding period alone.

- Capital losses must be applied against gains in a strict order (deferred gains first, then current gains; non-residential before residential within each). You can't simply choose to offset losses against whichever gain suits you best.

- Deductible gifts and donations can reduce the gain subject to the 30% minimum tax, but personal deductible super contributions generally can't reduce the tax below that 30% floor, and over-contributing can leave you worse off once contributions tax is factored in.

- A list of income-support payments (Age Pension, Disability Support Pension, JobSeeker, Parenting Payment, Youth Allowance, certain DVA and farm household payments) exempts recipients from the 30% minimum tax.

- Superannuation funds, including SMSFs, are unaffected and keep their existing one-third discount.

- Eligible new-build residential property gets a choice between the old 50% discount or the new indexation method at the time of sale.

New since our May update: the Government has agreed to remove the Minister's power to expand the list of CGT-discount-eligible asset classes by legislative instrument alone. Any future expansion now needs to pass through Parliament.

Talk to your accountant and adviser about: whether the loss-ordering rules change your strategy for realising losses, and whether any planned super contributions in a year you also realise a large indexed gain will actually produce a net benefit.

Can I still negatively gear my investment property?

Start date: 1 July 2027 (transition from 12 May 2026) - now law (pending assent) Urgency: 🔴 High

For established property purchased after Budget night (7.30pm AEST, 12 May 2026), the answer changes from 1 July 2027. From that date, losses on those properties can only be offset against rental income or capital gains from residential property, not against wages or other income.

Confirmed details:

- Properties owned (or under contract) before Budget night are grandfathered under current rules until sold.

- Properties bought between Budget night and 30 June 2027 can still be negatively geared against other income until that date, then the new rules apply.

- New-build properties remain fully eligible for negative gearing against any income.

- Super funds (including SMSFs) and widely held trusts are excluded from the restriction.

- Excess quarantined losses carry forward and offset future residential rent and capital gains.

- Other asset classes ie. shares, ETFs, commercial property are unaffected.

- If you move out of a pre-Budget-night main residence and rent it out after 1 July 2027, the quarantining rules don't apply to that property. However, only interest on the original loan balance remains deductible; any further borrowing against it is treated separately.

New since our May update: the Government has also given up the discretionary power to add further classes of negative-gearing-eligible property by Ministerial instrument alone, future expansions need to pass Parliament, the same change made on the CGT side. Media reports also indicate the Government intends to legislate protection for jointly owned properties that transfer to a co-owner on death or divorce, so the existing owner doesn't lose access to the pre-2027 discount or negative gearing eligibility, but this isn't locked in yet.

Talk to your accountant and adviser about: any plans to buy an established investment property, and whether your existing ownership structure (personal name, SMSF, or trust) still makes sense given which entities are excluded from the restriction.

What happens to my SMSF if I want to borrow against a property?

Start date: 45 days after Royal Assent Urgency: 🔴 High for SMSF trustees considering borrowing

This is new since our last update, it wasn't part of the original Budget announcement. It was added as a late Senate amendment in exchange for Greens support to pass the Bill. SMSFs will be prohibited from entering new limited recourse borrowing arrangements (LRBAs) to acquire residential property. LRBAs for genuine business real property are unaffected.

Key details:

- Existing LRBAs already in place are grandfathered and unaffected.

- Refinancing of a pre-commencement borrowing is also carved out.

- Acquisitions already under contract before commencement are protected, even if settlement falls afterwards.

- The ban starts just 45 days after the amending Act receives Royal Assent, a short window.

Talk to your financial adviser about: if an SMSF LRBA for residential property has been on your radar, this is genuinely time-critical. The window to enter a new arrangement is closing fast, and unlike most of the changes in this update, there's no multi-year runway here.

Are discretionary trusts being taxed differently? (Discretionary Trust Tax 2028 Update)

Proposed start date: 1 July 2028 Urgency: 🟡 Moderate (review before July 2028)

Not yet, and this is an important distinction from the measures above. Legislation for the discretionary trust changes has not been introduced to Parliament. The Government has indicated it will consult further before bringing this to Parliament later this year. The proposal, as it currently stands:

- Trustees pay a 30% minimum tax; non-corporate beneficiaries get a non-refundable credit; corporate beneficiaries ("bucket companies") don't, which revives the double-taxation issue for that structure.

- Fixed trusts, super funds, deceased estates, special disability trusts and charitable trusts are excluded, as is primary production income and income of vulnerable minors.

- Discretionary testamentary trusts holding assets they already held at announcement are exempt, but this exemption is not expected to extend to assets such trusts acquire afterwards, so estate plans using testamentary trusts may need review.

- Rollover relief is proposed to allow restructuring into a company or fixed trust over a three-year window.

Talk to your accountant about: whether your trust structure (or your testamentary trust provisions) would benefit from review once draft legislation is released. There's no need to act immediately, but it's worth getting ahead of before 2028.

What counts as a "new build" for tax purposes?

Urgency: 🟡 Moderate for anyone relying on the new-build exemptions

Both the CGT and negative gearing new-build exemptions hinge on a definition that hasn't been finalised yet, it will come via a separate legislative instrument. What we know so far:

- Construction on vacant land, and redevelopments that increase housing supply (for example, a single dwelling replaced by a duplex, townhouses or strata apartments), are expected to qualify.

- A single dwelling knocked down and rebuilt as a single dwelling is unlikely to qualify, as it doesn't add housing supply.

- Renovations or extensions to an existing property, including adding a granny flat, won't qualify.

The Government has also flagged further consultation on the precise definition, and on which types of "exempt housing investment" (such as affordable housing) might sit outside the negative gearing and CGT discount limits altogether.

Talk to your accountant about: any redevelopment plans for an investment property. Whether it qualifies as a "new build" can materially change the tax outcome.

Has anything changed for small business owners?

Start date: 1 July 2027 Urgency: 🟡 Moderate for business owners

Yes, and this one's easy to miss in the headlines. The turnover threshold for the small business 50% active asset reduction increases from $2 million to $10 million. This significantly widens the pool of business owners who can access this CGT concession when selling active business assets.

Talk to your accountant about: whether your business now qualifies under the higher threshold, and how this concession interacts with the broader CGT changes above.

What about the Working Australians Tax Offset and the $1,000 deduction?

Urgency: 🟢 Low

Two smaller measures are also now law (pending assent), with no change from what we reported in May:

- Working Australians Tax Offset (WATO): a new $250 non-refundable tax offset for resident individuals earning labour income (wages or sole trader income), from 1 July 2027, applied automatically through the tax return.

- $1,000 standard deduction: eligible workers can claim up to $1,000 in work-related expenses without receipts, from this financial year (1 July 2026). Donations, union fees and professional memberships can still be claimed on top.

Do I need to do anything right now?

For most people, no urgent action is required today, but a few specific situations genuinely are time-sensitive:

- Considering an SMSF property loan? The window to set up a new LRBA for residential property closes 45 days after Royal Assent. This is the most urgent item in this update.

- Holding assets with large unrealised capital gains? Talk to your accountant about the loss-ordering rules and the 1 July 2027 indexation split before that date arrives.

- Weighing up an established investment property purchase? The negative gearing rules already changed from Budget night. This isn't a future change, it's already in effect for new purchases.

- Running a business near the old $2 million turnover threshold? Check whether the new $10 million threshold opens up small business CGT concessions you didn't previously qualify for.

- Operate a discretionary trust, or have testamentary trust provisions in your will? Nothing to action today, but worth flagging for review once trust legislation is released later this year.

We'll be reaching out directly to clients where we think these changes are particularly relevant to their situation. In the meantime, if anything above has raised a question, get in touch, we're happy to talk it through.

This article is general information only and does not constitute financial advice. All measures described are based on Bills that have passed Parliament but, at the time of writing, await Royal Assent, as well as proposals yet to be legislated. These may change. Please consult your financial adviser and accountant before making any decisions.

P3 Financial Planning is a Brisbane-based financial advice practice helping clients across Australia navigate retirement planning, SMSF strategy, and tax-effective investing.